Debt collection scams have become increasingly sophisticated, targeting vulnerable consumers with aggressive tactics and fraudulent claims. These scammers exploit fear and urgency to extract money from individuals who may not even owe the alleged debt. Understanding how debt collection scams work, recognizing the warning signs, and knowing your rights are essential steps in protecting yourself from these predatory schemes. This comprehensive guide will equip you with the knowledge needed to identify fake debt collectors and take appropriate action when confronted with suspicious collection attempts.

Understanding Debt Collection Scams

Debt collection scams occur when fraudulent individuals or organizations impersonate legitimate debt collectors to deceive consumers into paying money they don’t actually owe. These scammers often use intimidation, threats, and false legal claims to pressure victims into making immediate payments. Unlike legitimate debt collection agencies that must follow strict federal regulations, scam debt collectors operate outside the law, employing tactics designed to confuse and frighten their targets.

How Do Debt Collection Scams Work?

Scammers obtain personal information through data breaches, public records, or underground markets. Armed with your name, phone number, and sometimes partial financial details, they contact you claiming you owe money for medical bills, payday loans, credit cards, or government obligations. They create urgency by threatening immediate legal action, wage garnishment, or arrest. Similar to how forex scams target investors with promises of high returns, debt collection scammers exploit psychological pressure and information asymmetry to bypass rational decision-making.

10 Red Flags That Indicate a Debt Collection Scam

Recognizing the warning signs of debt collection fraud can save you from financial loss and identity theft. Here are the most common indicators that you’re dealing with a scammer rather than a legitimate debt collector:

1. Refusal to Provide Written Verification

Legitimate debt collectors must send a written validation notice within five days of first contact, detailing the amount owed, the creditor’s name, and your rights to dispute the debt. Scam debt collectors will refuse to send written documentation or provide vague, incomplete information when pressed for details.

2. Demands for Immediate Payment

Fake debt collectors create artificial urgency, insisting you must pay immediately to avoid arrest or legal consequences. They may demand payment through wire transfers, prepaid debit cards, gift cards, or cryptocurrency – payment methods that are virtually untraceable and strongly suggest fraud. Legitimate collectors accept standard payment methods and provide reasonable timeframes for payment.

3. Threats of Arrest or Imprisonment

Threats of immediate arrest or jail time are definitive indicators of fraud. Is it illegal for debt collectors to threaten jail? Absolutely. You cannot be imprisoned for owing consumer debt. Can debt collectors threaten you with arrest? No – this violates federal law. While legitimate collectors can pursue lawsuits or wage garnishment, they cannot threaten criminal action.

4. Vague or Inconsistent Information

Scammers provide inconsistent or evasive answers when asked about the debt’s origin, the original creditor, or specific account details. They may become aggressive when questioned or refuse to provide verification information.

5. Aggressive or Abusive Behavior

Harassment by fake debt collectors includes repeated calls throughout the day, profanity, threats of violence, or contacting family members, employers, or neighbors about your alleged debt. The Fair Debt Collection Practices Act (FDCPA) prohibits such behavior from legitimate collectors.

6. Requests for Personal Information

Scammers may ask for your Social Security number, bank account details, or other sensitive information under the guise of “verifying your identity” or “processing your payment.” Much like what are phishing scams and how they work, these requests are designed to steal your identity rather than collect legitimate debt. A real debt collector already has your account information and doesn’t need you to provide basic identifying details.

7. Unfamiliar Debt Claims

The collector contacts you about a debt you’ve never heard of, from a creditor you don’t recognize, or for services you never used. While it’s possible to forget old debts or have debts sold to collection agencies, completely unfamiliar claims warrant thorough verification before any payment is made.

8. Spoofed or Hidden Caller ID

Debt collection robocalls often use caller ID spoofing to make their calls appear to come from government agencies, law enforcement, or legitimate companies. The number displayed may be local to your area code or show generic information like “Unknown” or “Private.” Legitimate collectors typically have consistent, verifiable phone numbers.

9. Pressure to Act Quickly

Scammers use high-pressure tactics, claiming that special settlement offers expire within hours or that legal action will commence immediately unless you pay right now. This urgency is designed to prevent you from thinking critically, researching the debt, or consulting with advisors. Legitimate debt collection involves formal procedures with reasonable timelines.

10. Suspicious Email Communications

Phishing debt collection emails contain suspicious attachments, request you click on links to “verify your account,” or contain grammatical errors and unprofessional formatting. These emails may appear to come from well-known companies but use slightly altered domain names or free email services. Identity theft and debt scams often begin with these fraudulent emails designed to harvest your personal information.

A Step-by-Step Guide to Identifying Legitimate vs. Fake Debt Collectors

How to verify a debt collector is a critical skill that every consumer should develop. The process of distinguishing between legitimate collection agencies and scammers requires systematic verification and documentation. Follow these essential steps to protect yourself:

Step 1: Request Written Validation

Never provide payment or personal information during the initial contact. Instead, request that the collector send written validation of the debt. Under the FDCPA, collectors must provide a validation notice that includes the amount owed, the name of the creditor, and a statement of your right to dispute the debt within 30 days. Legitimate collectors will comply without hesitation; scammers will typically refuse or become defensive.

Step 2: Verify the Collection Agency

Once you have the collection agency’s name, independently verify its existence. Search for the company online, check your state’s Attorney General’s office, or Better Business Bureau for complaints. Never use contact information provided by the caller—look up the company independently.

Step 3: Contact the Original Creditor

Reach out directly to the company that allegedly issued the debt using contact information from your records or their official website. Ask if they sold the debt to a collection agency and verify the agency’s name matches what you were told.

Step 4: Check Your Credit Reports

Are debt collection calls real or fake? Your credit report provides crucial evidence. Obtain free copies from all three major bureaus through AnnualCreditReport.com. If the debt is legitimate and sent to collections, it should appear on at least one credit report. Credit report scam alerts can also indicate fraudulent account activity.

Step 5: Document Everything

Keep detailed records of all communications with the collector. Note the date, time, caller’s name, company name, phone number, and a summary of the conversation. Save any emails, voicemails, or written correspondence. This documentation is essential if you need to report the scammer or if disputes arise. If you suspect a Collection broker is misleading you, thorough documentation becomes your primary defense mechanism.

Understanding Your Rights Against Debt Collection Scams

Consumer protection against debt scams begins with understanding your legal rights. The Fair Debt Collection Practices Act provides comprehensive protections against abusive collection practices, whether from legitimate agencies or scammers:

Protection from Harassment

Debt collectors cannot call repeatedly with the intent to harass, use profane language, threaten violence, or publish lists of non-paying consumers. They cannot call before 8 a.m. or after 9 p.m. without permission, and must stop contacting you if you send a written cease communication request.

Right to Dispute and Privacy Protections

You have 30 days from receiving the validation notice to dispute the debt in writing. Once disputed, collection efforts must cease until verification is provided. Collectors cannot discuss your debt with unauthorized third parties except to obtain location information. They’re also prohibited from lying about amounts owed, falsely claiming to be attorneys or government representatives, or threatening illegal actions. Can a scam debt collector sue you? While legitimate collectors can pursue lawsuits, scammers typically cannot and won’t follow through because they lack legitimate claims and fear exposure.

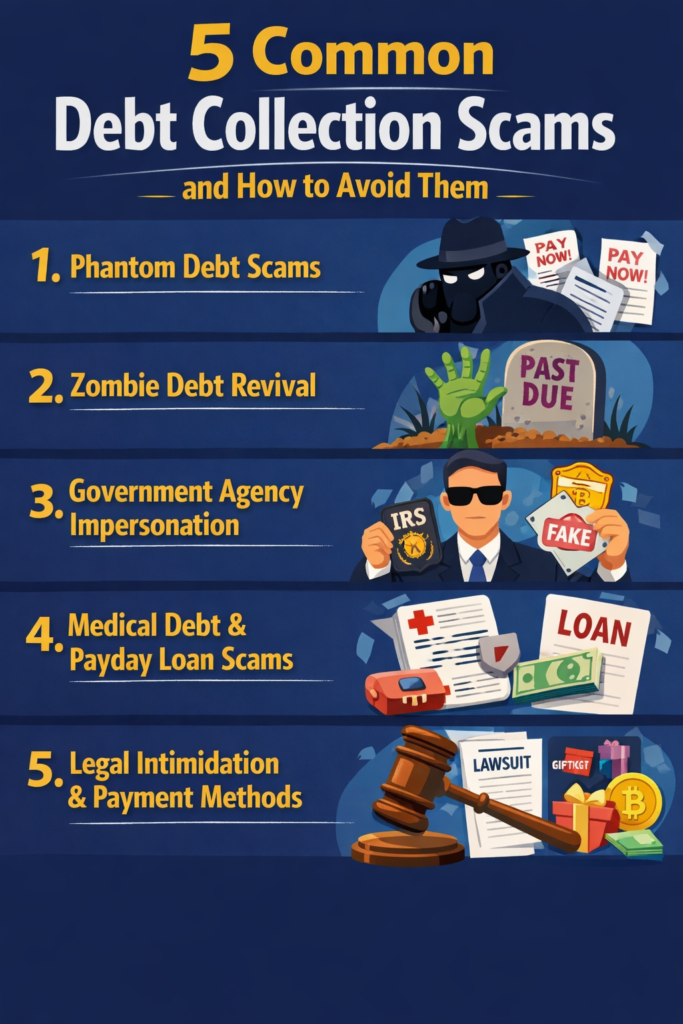

5 Common Debt Collection Scams and How to Avoid Them

Understanding the specific types of scams helps you recognize and avoid them. Here are the most prevalent debt collection fraud schemes:

1. Phantom Debt Scams

Scammers contact you about debts that never existed, claiming you owe money for services never used or loans never taken out. They rely on confusion and the possibility that you might have forgotten an old debt. Always verify any debt claim before payment.

2. Zombie Debt Revival

Scammers target old debts past the statute of limitations. By making you acknowledge the debt or make a small payment, they attempt to “revive” it and reset the limitations period. Never acknowledge ownership of a debt without first verifying its validity and checking if it’s time-barred.

3. Government Agency Impersonation

Fraudsters pose as IRS agents, Social Security officials, or law enforcement, claiming you owe taxes or fines. They use official-sounding titles and aggressive tactics. Government agencies send written notices before making phone contact and never demand payment via wire transfer or gift cards.

4. Medical Debt and Payday Loan Scams

Scammers exploit complex medical billing or claim you owe money on payday loans you never completed. Medical debt fraud is effective because healthcare billing is confusing. Payday loan scammers target people who applied online and may have partial information from applications or data breaches. Similar to the ultimate guide to avoiding bitcoin scams, protecting yourself requires verifying all claims before payment.

5. Legal Intimidation and Payment Method Scams

Scammers create fake legal documents, use official-sounding legal jargon, and threaten immediate lawsuits. They may claim to be attorneys and provide fake case numbers. These tactics panic victims into paying without verification. Additionally, fraudsters insist on untraceable payment methods – wire transfers, prepaid cards, gift cards, or cryptocurrency. How to report cryptocurrency scams effectively becomes crucial when scammers demand digital currency payments, as these transactions are difficult to reverse or trace.

5 Steps to Take if You Encounter a Debt Collection Scam

What to do if a scam debt collector calls requires immediate, decisive action to protect yourself and help authorities combat these fraudsters:

Step 1: Do Not Engage or Provide Information

If you suspect you’re speaking with a scammer, end the conversation immediately. Do not confirm any personal information, make any payments, or promise to call back. Scammers use information you provide to make their scams more convincing in future attempts. Simply hang up and block the number.

Step 2: Document the Contact

Write down the phone number, the caller’s name and company, claimed debt details, threats made, and payment methods requested. Save any emails or texts. This documentation supports your report and helps identify scam patterns.

Step 3: Verify Before Any Action

Check your credit reports, contact alleged creditors directly, and search online for the collection agency. Essential tips for identifying romance scams teach us that emotional manipulation and urgency are common threads – debt collection fraud uses fear instead of affection, but the verification principle remains the same.

Step 4: Report the Scam

How to report a debt collection scam involves notifying the Federal Trade Commission (FTC), Consumer Financial Protection Bureau (CFPB), your state Attorney General, and local police if threats were made. Each report contributes to enforcement efforts.

Step 5: Protect Your Accounts

If you provided personal or financial information, place fraud alerts on your credit reports, monitor statements for unauthorized charges, consider freezing your credit, and change compromised passwords.

How to Stop Fake Debt Collectors from Contacting You

Taking proactive measures can significantly reduce unwanted contact. Send a written cease and desist letter via certified mail demanding they stop contacting you. While scammers may ignore this, it creates a paper trail. Block phone numbers and use call-blocking apps that filter known scam numbers. Limit personal information exposure online by reviewing privacy settings and opting out of data broker websites. Monitor your credit regularly through free monitoring services to detect fraudulent accounts early.

Where Do I Report Fake Debt Collectors?

Reporting bill collection scams effectively is crucial for protecting yourself and others from fraudulent collectors. TruClaim provides a comprehensive platform specifically designed to help victims document, organize, and report debt collection fraud efficiently. The platform guides you through the entire reporting process, ensuring your complaint includes all necessary details and reaches the appropriate authorities.

When you file a complaint through TruClaim, the platform helps you organize evidence systematically, including call records, email communications, payment requests, and threatening messages. This organized documentation strengthens your case and provides investigators with clear, actionable information. The service acts as a centralized hub for all your fraud-related documentation, making it easier to track your case and follow up with authorities.

The Rise of Debt Collection Scams: What You Need to Know

Debt collection fraud has escalated dramatically in recent years. Automated dialing systems and caller ID spoofing enable scammers to contact thousands daily with minimal effort. Large-scale data breaches provide authentic personal information that makes schemes more convincing – stolen data trades on dark web marketplaces, continuously supplying scam operations. Economic pressures increase vulnerability as financially stressed individuals are more likely to believe they overlooked a debt. Understanding types of scams and their common patterns helps build resilience. Low prosecution rates due to international operations and anonymization techniques embolden criminals, making prevention and education critical for consumer protection.

Debunking Myths About Debt Collection Scams

Several misconceptions persist, making people more vulnerable to fraud.

Myth: “If they know personal information, they must be legitimate.”

Reality: Scammers obtain information through data breaches and public records. Knowing your details doesn’t make them legitimate – always verify independently.

Myth: “Making a small payment will make them go away.”

Reality: Paying confirms you’re a willing target and may restart the statute of limitations on legitimate but time-barred debts.

Myth: “Legitimate collectors never use aggressive tactics.”

Reality: Some unethical legitimate collectors do violate the FDCPA. Aggressive behavior warrants verification and potential reporting.

Myth: “I can’t be scammed because I have no debts.”

Reality: Scammers invent debts entirely, relying on confusion and fear rather than actual financial obligations.

Understanding what are phishing scams and how do they work reveals similar patterns of deception across different fraud types.

The Impact of Debt Collection Scams on Consumers

The consequences extend far beyond immediate financial loss. Victims often pay hundreds or thousands for non-existent debts, triggering cascading problems like missed legitimate payments, bank overdrafts, or inability to afford necessities. When scammers obtain personal information, they often commit identity theft, leading to fraudulent accounts and unauthorized credit inquiries. The harassment and intimidation cause significant emotional distress – anxiety, depression, sleep problems, and relationship strain. Fear of arrest or legal action creates lasting psychological trauma. Credit collection scams also erode consumer trust in legitimate financial systems, making victims suspicious of all collection attempts, potentially causing them to ignore real financial obligations.

Take Action to Protect Yourself and Others

If you’ve encountered suspicious debt collection activity or believe you may have been targeted, reporting the incident is essential. Your report contributes to patterns that help law enforcement identify and prosecute scam rings. Document every interaction carefully – dates, times, phone numbers, names used, threats made, and payment methods requested. This information strengthens your report and provides investigators with actionable intelligence.

TruClaim provides a secure platform where you can file detailed complaints about debt collection scams and other fraudulent activities. The service helps organize your evidence, guides you through the reporting process, and ensures your complaint reaches appropriate authorities. Whether dealing with fake debt collectors, phishing attempts, or other financial fraud, having a centralized place to document and report your experience is invaluable.

Remember that seeking guidance doesn’t mean you’ve failed – fraud can happen to anyone. Scammers are professionals who exploit universal human vulnerabilities like fear and urgency. Share this knowledge with family members, friends, and colleagues. Older adults are particularly vulnerable, and young people may lack the experience to recognize sophisticated tactics.

If you’re currently facing withdrawal issues with financial services, experiencing pressure from suspicious collectors, or have doubts about any debt claim, don’t wait to seek clarity. Taking immediate action to verify, document, and report protects your financial security and contributes to the broader fight against consumer fraud. The battle against debt recovery scams requires collective effort. Every report filed, every scam exposed, and every person educated makes these criminal operations less profitable and more risky.

For more updates, follow us on: